简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

GEMFOREX - weekly analysis

Abstract:The week ahead: Top 5 things to watch

U.S. inflation figures and the start of corporate earnings season will be the main highlights of an otherwise quiet week on the economic calendar.

Inflation data for December will help influence the size of the Federal Reserves next rate hike, while corporate earnings will give an important insight into the health of the economy amid concerns over a potential slowdown.

UK GDP, Japanese inflation, and Eurozone data will also be in focus.

1) U.S. CPI

The U.S. consumer price index for December is due out on Thursday with economists expecting core inflation to have increased 5.7% from a year earlier. Any sign that price pressures are continuing to ease could not only reinforce the view that the Fed is nearing the end of its most aggressive tightening cycle in decades, but may also fuel speculation for further rate cuts later this year.

U.S. data on Friday showed that December payrolls expanded more than expected even as wage increases slowed and services activity contracted, easing worries about the Feds monetary policy path.

Fed officials on Friday acknowledged cooling wage growth and other signs of a gradually slowing economy, with Atlanta President Raphael Bostic hinting at the chance of a quarter percentage point hike at the Feds next policy meeting on Jan. 31 – Feb. 1. It raised rates by 50 basis points in December.

2) Earnings season gets underway

Companies are due to start reporting fourth quarter earnings in the coming week, with investors looking for signs of a potential economic slowdown filtering through to bottom lines.

On Friday alone, reports are due from banks Wells Fargo (NYSE:WFC), Citigroup (NYSE:C), Bank of America (NYSE:BAC) and JPMorgan (NYSE:JPM), healthcare titan UnitedHealth Group (NYSE:UNH), asset manager BlackRock (NYSE:BLK) and Delta Air Lines (NYSE:DAL).

Consensus analyst estimates call for a 1.6% decline in S&P 500 Q4 earnings versus the year-ago period, according to Refinitiv IBES. Some reckon 2023 projections are still too rosy given recession risks.

Stocks may be more expensive than they appear if current earnings estimates do not fully account for any economic slowdown, while any downturn could further dampen what investors are willing to pay for equities.

3) U.K. GDP

The U.K. is to release November GDP figures on Friday against a background of a historic cost-of-living squeeze amid double digit levels of inflation, transport and public sector strikes and a softening housing market as the country faces what is likely to be a lengthy recession.

Following nine consecutive rate rises by the Bank of England, and more to come, British mortgage approvals plumbed their lowest level in November since the pandemic-induced slump of June 2020, recent data showed.

As price pressures and higher borrowing costs bite, Prime Minister Rishi Sunak has pledged to cut inflation in half, grow the economy, reduce public debt and cut health service waiting lists.

However, analysts at Deutsche Bank see high inflation persisting this year, no rate cuts until 2024 and fiscal policies becoming more austere, while analysts at Barclays expect the UK economy to keep contracting until the end of the third quarter of 2023.

4) Eurozone data

Germany is to publish an estimate of annual GDP growth on Friday, which will show the impact of the energy crisis triggered by Russia‘s war in Ukraine on the Eurozone’s largest economy.

The broader Eurozone is to publish data on industrial production and trade the same day. The high costs of energy imports have flipped the blocs trade balance from surplus to deficit, but the deficit reduced in October as gas prices eased and market watchers will be looking to see if this trend continued in November.

Industrial production is forecast to make a small rebound after a decline in October.

5) Tokyo inflation

Market watchers will be keeping a close eye on Tokyo's inflation numbers on Tuesday, after last month's report first tipped the market to a potential Bank of Japan policy shift.

Tokyo CPI - which front-runs the national numbers, often by several weeks - surged to a four-decade high in November.

Less than a month later, the BOJ tweaked its bond-yield control that allows long-term interest rates to rise more, wrong-footing markets. The move was aimed at easing some of the costs of prolonged monetary stimulus.

The yen has strengthened to seven-month highs on rising expectations for a further hawkish shift, even as BOJ officials maintain the move was a one-off. The BOJ is due to hold its next policy meeting on Jan. 18

Lastly, here are some key assets to keep an eye on in the week that has just commenced:

WTI US Oil

WTI grinds higher near the intraday top surrounding $74.70 as firmer sentiment jostles with economic slowdown concerns during early Monday. Even so, the softer US Dollar and a light calendar allow the black gold buyers to keep the reins, after Fridays mixed performance.

EURUSD

EUR/USD is holding on to the upside below 1.0700 in the early European trades. The pair is taking advantage of the extended weakness in the US Dollar amid hopes of a dovish Fed pivot and China's reopening optimism. Eurozone data awaited.

The Relative Strength Index (RSI) indicator on the four-hour chart stays near 60, suggesting that EUR/USD has more room on the upside before turning technically overbought.

1.0700 (static level, broken ascending trend line) aligns as first resistance. Once EUR/USD rises above that level and starts using it as support, it could target 1.0735 (December 15 high) and 1.0800 (static level, psychological level) afterward.

On the downside, 1.0620 (50-period Simple Moving Average (SMA), 100-period SMA) could be seen as first support before 1.0600 (psychological level, 20-period SMA, static level) and 1.0560 (200-period SMA).

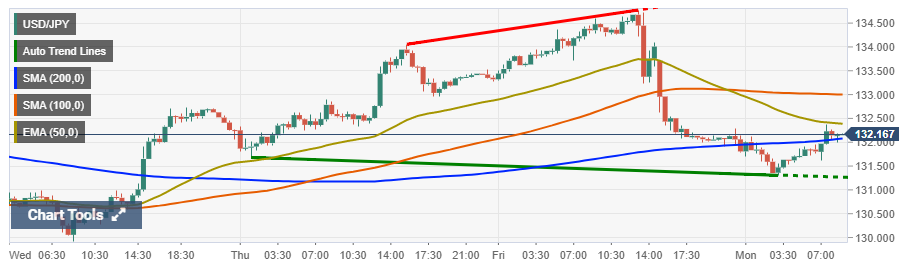

USDJPY

The USD/JPY pair struggles to gain any meaningful traction on the first day of a new week and seesaws between tepid gains/minor losses through the early European session. The pair is currently placed just below the 132.00 round-figure mark and seems vulnerable to extending Friday's retracement slide from over a one-week high.

The USD/JPY pair builds on this week's recovery move from mid-129.00s, or its lowest level since June 2022 and gains traction for the fourth successive day on Friday. The momentum lifts spot prices to over a one-week high, around the 134.40 area during the early part of the European session and is sponsored by a strong follow-through US Dollar buying.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

GemForex | Crude Oil (WTI)

Crude Oil (WTI) - Rebound in the offing?

Japanese Yen Technical Analysis: EUR/JPY, CAD/JPY. What Happened to Momentum?

JAPANESE YEN, EUR/JPY, CAD/JPY - TALKING POINTS AND ANALYSIS

Japanese Yen Technical Analysis: USD/JPY, AUD/JPY. Are They Establishing Ranges?

JAPANESE YEN, USD/JPY, AUD/JPY - TALKING POINTS

WTI hits fresh cycle highs in the mid-$63.00s

WTI hits fresh cycle highs in the mid-$63.00s

WikiFX Broker

Latest News

Volkswagen agrees deal to avoid Germany plant closures

WikiFX

WikiFXGeopolitical Events: What They Are & Their Impact?

WikiFXTop 10 Trading Indicators Every Forex Trader Should Know

WikiFXTradingView Launches Liquidity Analysis Tool DEX Screener

WikiFXMultiBank Group Wins Big at Traders Fair Hong Kong 2024

WikiFXWikiEXPO Global Expert Interview: Simone Martin—— Exploring Financial Regulation Change

WikiFX'Young investors make investment decisions impulsively to keep up with current trends' FCA Reveals

WikiFXWhy Do You Feel Scared During Trade Execution?

WikiFXCySEC Settles Compliance Case with Fxview Operator Charlgate Ltd

WikiFXScope Markets Review: Trustworthy or Risky?

WikiFXCurrency Calculator