简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Implied Volatility: What is it & Why Should Traders Care?

Abstract:Implied Volatility: What is it & Why Should Traders Care?

Implied volatility, synonymous with expected volatility, is a variable that shows the degree of movement expected for a given market or security. Often labeled as IV for short, implied volatility quantifies the anticipated magnitude, or size, of a move in an underlying asset.

WHAT IS IMPLIED VOLATILITY?

Implied volatility is a number displayed in percentage terms reflecting the level of uncertainty, or risk, perceived by traders. IV readings, which are derived from the Black-Scholes options pricing model, can indicate the degree of variation expected for a particular equity index, stock, commodity, or major currency pair over a stated period of time.

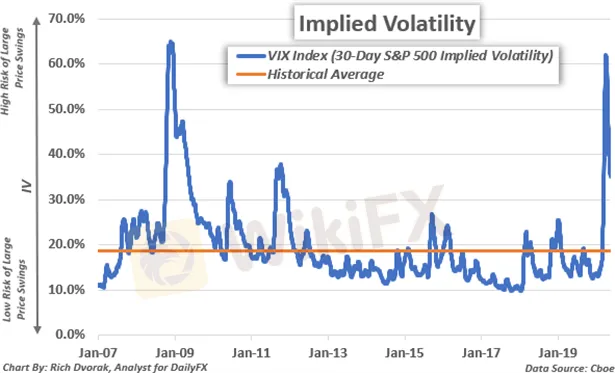

For instance, the popular VIX Index is simply the 30-day implied volatility reading for the S&P 500. A high VIX level (i.e. percent), or high implied volatility reading, indicates that risk is relatively elevated and there is a greater chance of larger than normal price swings.

IMPLIED VOLATILITY VS HISTORICAL VOLATILITY – WHAT IS THE DIFFERENCE?

Implied volatility is the expected size of a future price change. Implied volatility broadly reflects how big or small of a move is anticipated to be over a particular time frame. On the other hand, historical volatility, or realized volatility, indicates the actual size of a previous price change. Historical volatility illustrates the overall level of market activity that has already been observed.

The average true range (ATR) of an asset or security is an example of an indicator that illustrates historical volatility. Though implied volatility and historical volatility differ slightly in the regard of future expectations versus past observations, the two metrics are closely related and tend to move in similar patterns.

Implied volatility readings are typically higher when there is a large degree of uncertainty corresponding with potential for market impact – and often surrounds economic data releasesor other scheduled risk events like central bank meetings. This can lead to larger price swings and thus can materialize into higher readings of realized volatility. Likewise, when historical volatility remains anchored during calm market conditions, or when perceived risk is relatively subdued, IV tends to be lower.

IMPLIED VOLATILITY CAN REFLECT MARKET RISK AND UNCERTAINTY

Implied volatility is a projection of how much market movement is anticipated – regardless of the direction. In other words, implied volatility reflects the expected range of potential outcomes and uncertainty around how high or low an underlying asset might rise or fall.

High implied volatility indicates there is a greater chance of large price swings expected by traders whereas low implied volatility signals the market expects price movements to be relatively tame. Implied volatility measurements can also help traders gauge market sentimentconsidering IV broadly depicts the level of perceived uncertainty – or risk.

IMPLIED VOLATILITY TRADING RANGES CAN INDICATE TECHNICAL SUPPORT AND RESISTANCE LEVELS

Implied volatility measurements can be incorporated into various trading strategies as well. This is due to their usefulness for identifying potential areas of technical support and resistance. An implied volatility trading range is typically calculated under the assumption that prices will stay contained within a one-standard deviation move. Mathematically, this means that there is a 68% statistical probability that price action will fluctuate within the defined implied volatility trading range over a specified time frame.

That said, if prices trade at the upper barrier of its pre-defined implied volatility trading range, then there is an 84% statistical probability that prices will gravitate lower and a 16% probability that prices will continue rising. On the other hand, if prices trade at the lower barrier of its pre-defined implied volatility trading range, then there is an 84% statistical probability that prices will drift higher and a 16% probability that prices will continue falling.

ADVANTAGES OF IMPLIED VOLATILITY AS A FOREX SIGNAL

Largely owed to the inherent mean-reverting characteristic of major currency pairs, implied volatility trading ranges typically serve as robust forex signals. For example, this EUR/GBP analysisthat defined a 24-hour implied volatility trading range for EUR/GBP provided an illustrated example of how these technical barriers can help traders identify possible inflection points and trading opportunities.

On 14 January 2020, spot EUR/GBP price action was trading at 0.8541 and its implied volatility measurement was clocked at 7.3% for the overnight (i.e. 1-day) options contract. Using these value inputs, and the options-derived trading range formula below, it was estimated that EUR/GBP would fluctuate between implied support of 0.8508 and implied resistance of 0.8574 over the next 24-hours with a 68% statistical probability.

In other words, the calculated 24-hour trading range reflected a 1-standard deviation implied move of +/- 0.0033 from spot, which meant that Euro-Pound volatility was expected to be contained within a 66- pip band around its then-current price of 0.8541 for the 15 January 2020 trading session.

As trading progressed and market activity unfolded, EUR/GBP jumped to an intraday high of 0.8578, but the currency pair closed the 15 January 2020 session at 0.8547 after spot prices pivoted sharply lower. This was driven by an influx of selling pressure that followed a rejection of its implied high technical barrier.

USING IMPLIED VOLATILITY TO TRADE COMMODITIES, STOCKS, & INDICIES

In addition to forex, implied volatility gauges can be incorporated into trading strategiesfor commodities, stocks, and indices. As mentioned above, measures of implied volatility can indicate the markets overall level of uncertainty. Correspondingly, cross-asset implied volatility benchmarks tend to reflect useful relationships with their respective underlying markets and may provide insight as to where that market might head next.

Chart created by @RichDvorakFXwith TradingView

Arguably the most popular implied volatility benchmark is the S&P 500 VIX Index. The VIX Index typically rises amid turbulent market conditions and increasing uncertainty, though the ‘fear-gauge’ tends to soar during aggressive selloffs in stocks. In turn, the VIX generally holds a strong inverse relationship with the S&P 500.

The OVX Index, which reflects 30-day expected crude oil price volatility, provides an example of another commonly cited IV benchmark. Seeing that the price of crude oil and stocks react similarly to deteriorating risk appetite, it is unsurprising that sentiment-linked crude oil frequently maintains a negative correlation with both the VIX and OVX.

Chart created by @RichDvorakFXwith TradingView

Although this inverse relationship typically observed between an assets price and its implied volatility reading serves as a general rule of thumb, that is not always the case and there are certain exceptions. The correlation of price with implied volatility is dynamic, meaning it is constantly changing, which corresponds with a relative strengthening or weakening from their historical relationship.

Similarly, when it comes to common safe-haven assets, a direct relationship between price and implied volatility may show. For instance, the US Dollar Index (DXY) broadly follows the ebb and flow of expected currency volatility(FXVIX). Also, a positive correlation is often reflected by the price of gold and gold volatility (GVZ). These examples help illustrate the valuable insight that implied volatility readings can provide when incorporated into macro approaches and other comprehensive trading strategies.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

Easy Trading Online Awarded “Best Forex Broker - Asia” at Wiki Finance EXPO 2024 Hong Kong

We are thrilled to announce that Easy Trading Online has been awarded the “Best Forex Broker - Asia” at the Wiki Finance EXPO 2024 Hong Kong! This prestigious recognition underscores our commitment to excellence and dedication to providing top-notch services to our clients.

Celebrating Excellence of Easy Trading Online at 2024 FastBull Awards Ceremony

On the evening of April 28, Easy Trading Online proudly received the 'Most Trusted Forex Broker' award at the BrokersView 2024, hosted by Fastbull. This accolade is a testament to our steadfast dedication to providing reliable and superior trading services in the forex and CFD brokerage industry.

Easy Trading Online Shines as Gold Sponsor at BrokersView Expo Dubai 2024

The BrokersView Expo Dubai 2024 is a premier event in the financial industry, bringing together top financial institutions, brokers, and technology providers from around the globe. As the Gold Sponsor of BrokersView Expo Dubai 2024, Easy Trading Online took the opportunity to showcase our latest products, service technologies, and core competitive advantages in the forex trading field.

Easy Trading Online at the Wiki Gala Night

On the 23rd of March, the Easy Trading Online family had the distinguished pleasure of being the Table Sponsor at the prestigious Wiki Gala Night. As we reflect on the event, it’s with a sense of pride and joy that we share the highlights and our takeaways from an evening that was as inspiring as it was splendid.

WikiFX Broker

Latest News

Elderly Trader Loses RM2.1M in WhatsApp Forex Scam

WikiFX

WikiFXSpotware Unveils cTrader Store, Global Marketplace for Algo Creators

WikiFXGigamax Scam: Tracking Key Suspects in RM7 Million Crypto Fraud

WikiFXWikiFX Review: Is IQ Option trustworthy?

WikiFXCFI Partners with MI Cape Town, Cricket Team

WikiFXDoo Financial Expands Reach with Indonesian Regulatory Licenses

WikiFX5 Questions to Ask Yourself Before Taking a Trade

WikiFXQuadcode Markets: Trustworthy or Risky?

WikiFXAvoid Fake Websites of CPT Markets

WikiFXWebull Canada Expands Options Trading to TFSAs and RRSPs

WikiFXCurrency Calculator