简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Europes Economy to Outpace U.S. in Upending of Past Roles

Abstract:The euro area economy is for once set for a sprightlier recovery from crisis than the U.S., thanks to starkly different responses to the coronavirus.

The euro area economy is for once set for a sprightlier recovery from crisis than the U.S., thanks to starkly different responses to the coronavirus.

Americas failure to get a grip on the pandemic is putting the brakes on its rebound compared with Europe, where many former virus hot spots managed to resume economic activity without causing a similar surge in infections.

Crucial for a sustainable recovery is confidence that the virus is no longer out of control, and Europes relative success may help encourage shoppers to spend and businesses to invest, further propelling demand and growth. The region has also done a better job of protecting jobs and incomes, at least for now, with furlough programs keeping millions of workers on payrolls.

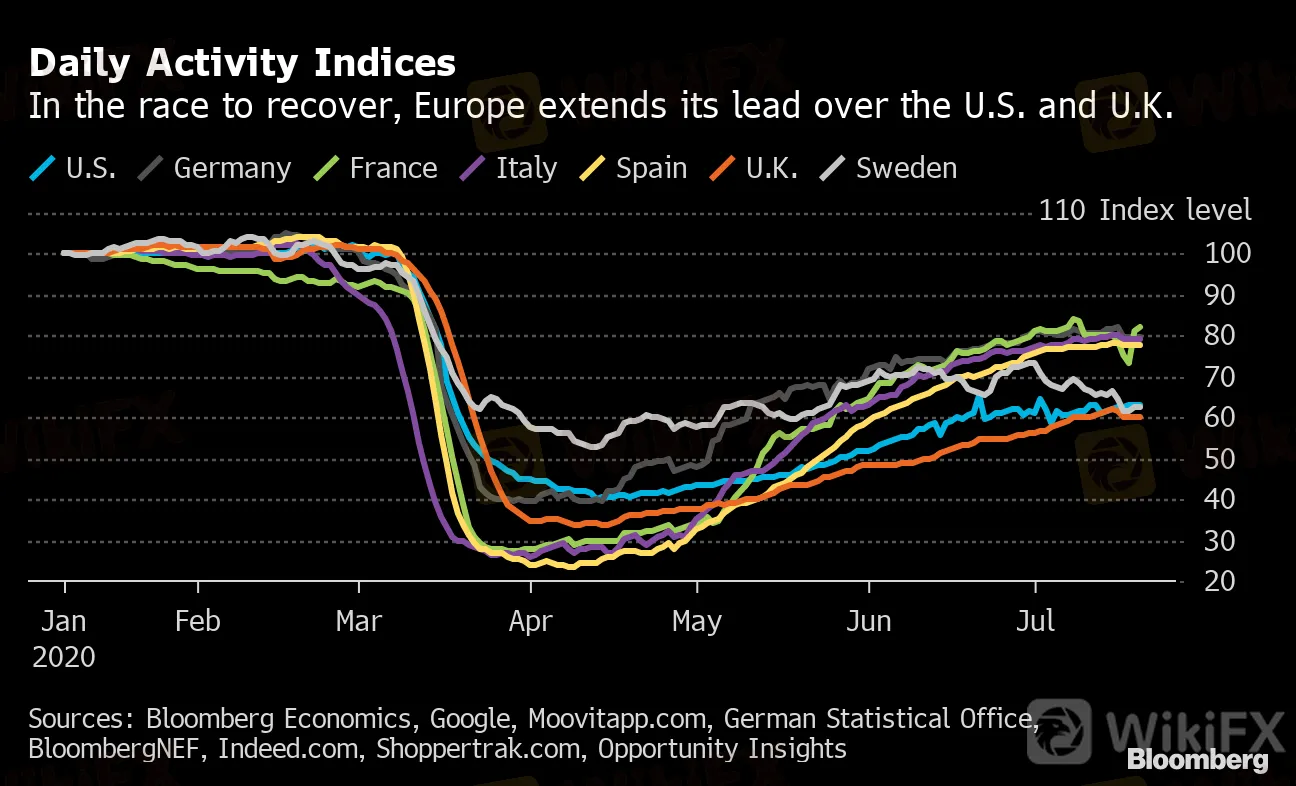

Daily Activity Indices

In the race to recover, Europe extends its lead over the U.S. and U.K.

Sources: Bloomberg Economics, Google, Moovitapp.com, German Statistical Office, BloombergNEF, Indeed.com, Shoppertrak.com, Opportunity Insights

According to JPMorgan Chase & Co., Europe will do better because it has “broken the chain” that links mobility and the virus. Goldman Sachs Group Inc. has cited effective virus control as one reason it expects a “steeper and smoother rebound in the euro area than elsewhere.”

“It‘s very clear that the euro area turned down more sharply but we also expect it to bounce back more sharply,” said Jari Stehn, chief European economist at Goldman Sachs. “It’s pretty rare that the euro area would outgrow the U.S. over a horizon of one to two years.”

Since 1992, the U.S. has outperformed the euro area in all but eight years, according to IMF data. Although the euro area managed to grow when the financial crisis hit in 2008 and the U.S. shrank, in 2009 the U.S. contraction of 2.5% was far shallower than the euro areas 4.5%.

Aggressive lockdowns mean the euro area is set for a sharper second-quarter contraction than the U.S., something that will be seen in GDP figures due this week.

The euro-area economy probably shrank 12% in the three months through June, according to a Bloomberg survey. The U.S. contraction, on an annualized basis, is forecast to be 35%, or a roughly 10% decline quarter-over-quarter.

But high-frequency data suggest Europe is on the mend faster, and Bloomberg Economics estimates that the lead has widened recently.

“Having been hit hardest it‘s pretty impressive that we think that Europe will recover more fully,” said Bruce Kasman, chief economist at JPMorgan. “They’ve broken that link -- the mobility numbers are going up” without a resurgence of the virus, thanks to better contract tracing, mask-wearing and social distancing measures, he said.

JPMorgan expects the euro area‘s economy to shrink 6.4% this year, slightly worse than the 5.1% contraction seen for the U.S. But for 2021, the bank forecasts a 6.2% rebound for the euro area, more than double America’s 2.8% growth.

In the U.S., a jump in cases across the South and West has led several states to halt or even reverse reopening plans. Measures of mobility and restaurant bookings have plateaued, and more than 1 million applications for unemployment benefits continue to be filed each week.

Read more: Euro Skeptics Are Now Believers And Its Driving Markets Higher

Meanwhile, euro-area purchasing managers indexes jumped more than forecast in July, while numbers for the U.S. came in lower than expected, especially for services, which make up a much larger part of the economy than manufacturing.

The U.S. economic situation could worsen if lawmakers dont extend -- in some form -- the extra $600 per week in unemployment benefits that have supported incomes and spending in recent months.

Senate Republican leader Mitch McConnell is set to release the GOPs proposal on Monday after the party and President Donald Trump squabbled last week over the details of the plan, giving Congress almost no time to avoid a lapse in the unemployment aid.

The divergence is reflected in markets. European stocks and bonds have benefited from renewed investor popularity, thanks to the blocs agreement on a historic 750 billion-euro ($860 billion) accord. The euro has risen more than 6% against the dollar in the past two months, and could have further to run.

In Europe, generous loan and furlough programs prevented an immediate surge in unemployment, which is also helping the near term. Many were modeled on Germanys renowned Kurzarbeit and largely proved efficient at getting aid to workers.

But it‘s early in the recovery phase, and countries can’t keep funding support indefinitely. If demand doesnt come back strong enough, companies may eventually have to cut costs, meaning Europe may only have delayed a damaging increase in joblessness.

Just because Europe is in a relatively better position to come out of this in the second half of the year, “doesn‘t mean the U.S. can’t catch up,” said Michael Gapen, chief U.S. economist at Barclays Plc.

In the U.S., the $2 trillion rescue package that Congress passed in March ranks among the most aggressive in history, but the distribution has been patchy and uneven. Unemployment offices were overwhelmed with claims, and many jobless Americans have still yet to receive the unemployment benefits theyre owed.

At the same time, the allocation of loans to small and medium-sized businesses had its own challenges, resulting in a chaotic scramble among business owners to get government assistance. Even so, the Paycheck Protection Program helped save as many as 3.2 million jobs, according to a study by Massachusetts Institute of Technology and Federal Reserve researchers.

High-frequency data suggests “things have stalled out, either because theres exhaustion of initial pent-up demand or because of the virus creating a change in consumer behavior,” said Michelle Meyer, head of U.S. economics at Bank of America Corp. While the third quarter will get a boost from initial state reopenings, “now the question is, how sustainable is that bounce?”

| Read More: |

|---|

|

— With assistance by Bjorn Van Roye, Zoe Schneeweiss, Brian Swint, and Michael Msika

(Adds GOP proposal in 15th paragraph)

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Geopolitical Events: What They Are & Their Impact?

WikiFX

WikiFXVolkswagen agrees deal to avoid Germany plant closures

WikiFXTop 10 Trading Indicators Every Forex Trader Should Know

WikiFXTradingView Launches Liquidity Analysis Tool DEX Screener

WikiFXMultiBank Group Wins Big at Traders Fair Hong Kong 2024

WikiFXWikiEXPO Global Expert Interview: Simone Martin—— Exploring Financial Regulation Change

WikiFX'Young investors make investment decisions impulsively to keep up with current trends' FCA Reveals

WikiFXWhy Do You Feel Scared During Trade Execution?

WikiFXCySEC Settles Compliance Case with Fxview Operator Charlgate Ltd

WikiFXMalaysian Influencer Detained in Taiwan Over Alleged Role in Fraud Scheme

WikiFXCurrency Calculator