简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Gold and U.S. Treasuries Cant Both Be Trusted

Abstract:A sharp reversal in these assets at the same time muddles the economic outlook.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

Read more opinion

Follow @BChappatta on Twitter

COMMENTS

LISTEN TO ARTICLE

5:05

SHARE THIS ARTICLE

Share

Tweet

Post

Gold meltdown.

Photographer: David Gray/AFP/Getty Images

Photographer: David Gray/AFP/Getty Images

Nothing gets Wall Street fired up quite like a sharp reversal in prevailing trends across markets.

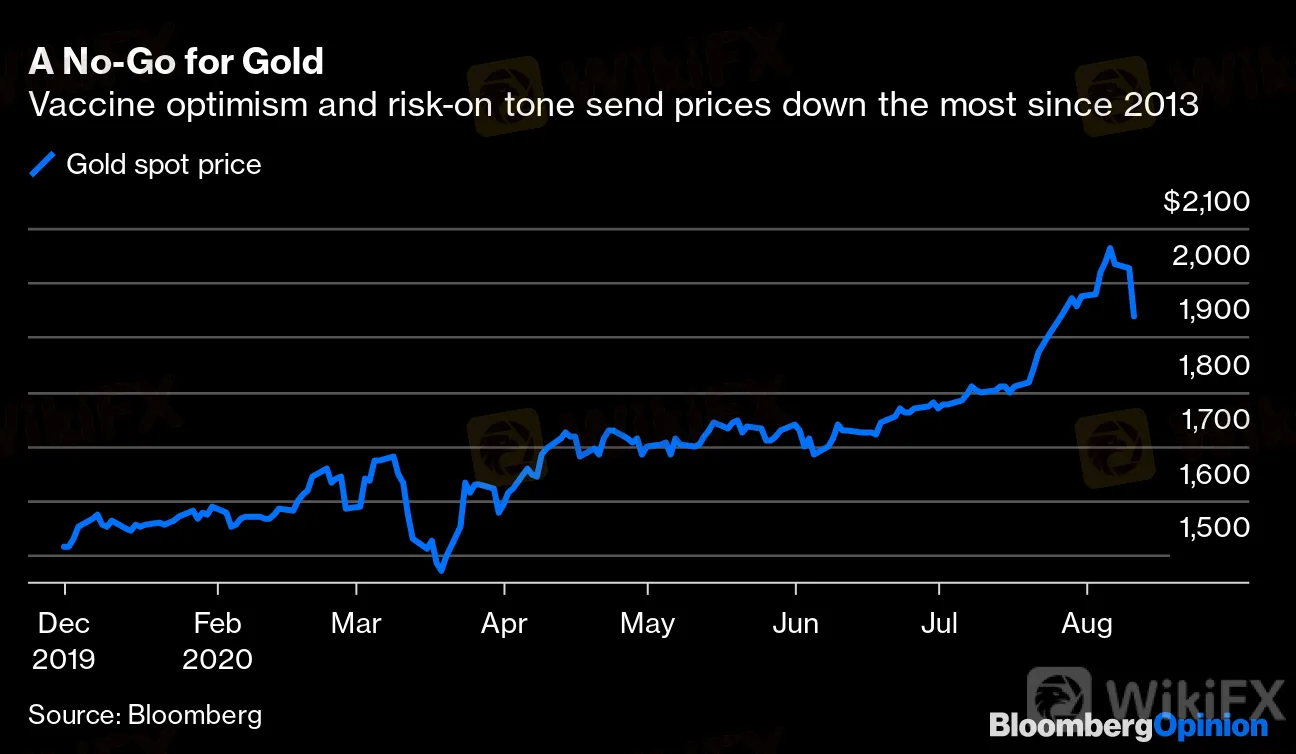

So the excitement in the air was palpable on Tuesday, with the price of gold tumbling by the most since 2013, yields on 30-year Treasuries jumping by the most in more than two months and industries like banks, energy and automobiles powering stocks higher instead of technology companies. The initial impetus for selling everything that was once in favor, and buying previously unloved assets, seemed to be Russia‘s announcement that it registered its first coronavirus vaccine (though there’s reason to be skeptical of it) and President Donald Trump‘s comments that he’s “seriously” considering a capital gains tax cut.

{18}

A No-Go for Gold

{18}

Vaccine optimism and risk-on tone send prices down the most since 2013

Source: Bloomberg

{777}

Another interesting piece of news came later, when a core measure of prices paid to U.S. producers accelerated in July for the first time in six months. The producer-price index excluding food and energy jumped by 0.5% from the previous month, the biggest increase since 2018 and easily topping estimates for a 0.1% gain. All together, it signals unexpected price pressure and raises the stakes for Wednesday‘s release of July’s consumer price index data, which is projected to show a decline in year-over-year core inflation for the fifth consecutive month.

{777}

Traders have been fixated on what comes next for inflation as they wrap their heads around the lasting effects of the coronavirus crisis and the ensuing response by policy makers around the world. In the U.S., the fear of a deflationary period has given way to expectations for a sustained pickup in price growth, given the flood of fiscal stimulus and signals from the Federal Reserve that it would tolerate — and perhaps even encourage — an overshoot of its 2% inflation target.

More from

{28}

Bidens Smart Pick for Vice President Tells Us a Lot

Recessions Lead People to Make Big Money Mistakes

How Far Will Chinas Surveillance State Stretch?

U.S. Goes It Alone to Keep Weapons Out of Iran

{28}

Given this context, Tuesday‘s selloff in gold and U.S. Treasuries is puzzling. Yes, both are classically considered “havens” and are prone to decline during bouts of “risk-on” trading. And it’s true that the Treasury Department is embarking on record-sized auctions of longer-dated securities this week, pressuring the U.S. government bond market.

But why would positive economic news and a strong PPI number spark a decline in assets like gold and Treasury Inflation Protected Securities, which are used as inflation hedges? My hunch is there‘s a “buy the rumor, sell the news” element at play now that there’s actual evidence of prices stabilizing so soon after the worst of the downturn.

Still, if you believe that the Fed has the power to bend financial markets to its will, these moves can‘t be trusted. As my Bloomberg Opinion colleague Tim Duy wrote this week, the Fed can always just expand its asset purchases to target the long-end of the yield curve to offset any additional issuance, which would depress term premiums and push investors into riskier assets. Given how much uncertainty remains about the economic recovery, and with inflation nowhere near the central bank’s desired level, it seems far too premature to wager that the Fed will even think about pumping the brakes on its easing measures. Chair Jerome Powell has signaled time and again that hed keep his foot on the gas until America was far past the pandemic.

Back from the Abyss

Long bond yields increased by the most in months

Source: Bloomberg

If thats the case, then why did gold plunge by more than 5%? The easy answer is that based on relative-strength index analysis, it was hugely overbought and is just now coming back to a more reasonable level. Yet the reasons behind its rally remain firmly in place. If the Fed will use all of its tools to keep benchmark Treasury yields near record lows while encouraging inflation to run hotter than before, then policy makers have all but guaranteed negative real yields for years to come. In a world in which the Fed unabashedly suppresses the U.S. yield curve, negative real yields could be interpreted as markets betting on a reflated American economy through higher prices for inflation-linked securities.

Now, it‘s always been hard to ascertain a “fair value” for an ounce of gold. Tuesday’s decline was “quite abrupt and brutal, but the price increase before was even more abrupt and brutal,” Carsten Fritsch, a commodity analyst at Commerzbank AG, told Bloomberg News‘s Justina Vasquez. Meanwhile, the Fed probably won’t provide explicit guidance for where it wants longer-dated Treasury yields, leaving traders mostly content to play the ranges of the past few months. Analysts at TD Securities, for their part, said on Tuesday that they would double down on long positions in 10-year notes.

Precise levels aside, I‘m skeptical that a tandem selloff in gold and Treasuries will gain much momentum. While I’d argue that the Fed is comfortable with Tuesdays increase in long-term U.S. yields to the extent that it reflects the better-than-expected producer price data, it seems likely that if rates continue to climb, at some point either financial markets will revolt, as they did in early June, or the central bank will step in and buy. While gold is a more fickle investment and has more room to tumble after its recent surge, sub-zero real yields should provide something of a floor and keep pensions and private-wealth managers open to owning it.

{43}

But most of all, it boils down to inflation and currency strength. If Americas dalliance with helicopter money causes persistent price growth to take hold and the dollar to weaken, then gold should set records. If this period of ultra-easy policy is yet another head-fake and the global economy recovers in fits and starts, then Treasuries should continue to be well-bid, both by private investors and the Fed. Whichever scenario wins out, these price swings are more likely to be flashes in the pan than something more permanent.

{43}

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Brian Chappatta at bchappatta1@bloomberg.net

To contact the editor responsible for this story:

Daniel Niemi at dniemi1@bloomberg.net

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Spotware Unveils cTrader Store, Global Marketplace for Algo Creators

WikiFX

WikiFXElderly Trader Loses RM2.1M in WhatsApp Forex Scam

WikiFXGigamax Scam: Tracking Key Suspects in RM7 Million Crypto Fraud

WikiFXSingaporean Arrested in Thailand for 22.4 Million Baht Crypto Scam

WikiFXTrader Turns $27 Into $52M With PEPE Coin, Breaking Records

WikiFXASIC Sues HSBC Australia Over $23M Scam Failures

WikiFXCFI Partners with MI Cape Town, Cricket Team

WikiFXDoo Financial Expands Reach with Indonesian Regulatory Licenses

WikiFXWikiFX Review: Is IQ Option trustworthy?

WikiFX5 Questions to Ask Yourself Before Taking a Trade

WikiFXCurrency Calculator