简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

The ECB Can't Slow Its Stimulus Buying Yet

Abstract:Europes economic recovery is still in its infancy. The bank has to be ready to provide more support, not less.

The European Central Bank has been at the forefront of the euro zone‘s economic response to the Covid-19 crisis. As political leaders scramble to conjure up a joint fiscal response, the central bank’s governing council can afford to stand still when it meets on Thursday.

Since the pandemic in Europe appears relatively contained, some central bankers may find it tempting to discuss when and how to begin withdrawing emergency stimulus measures. President Christine Lagarde should ignore such suggestions: The ECB has to continue supporting the economy and be ready to do even more if needed.

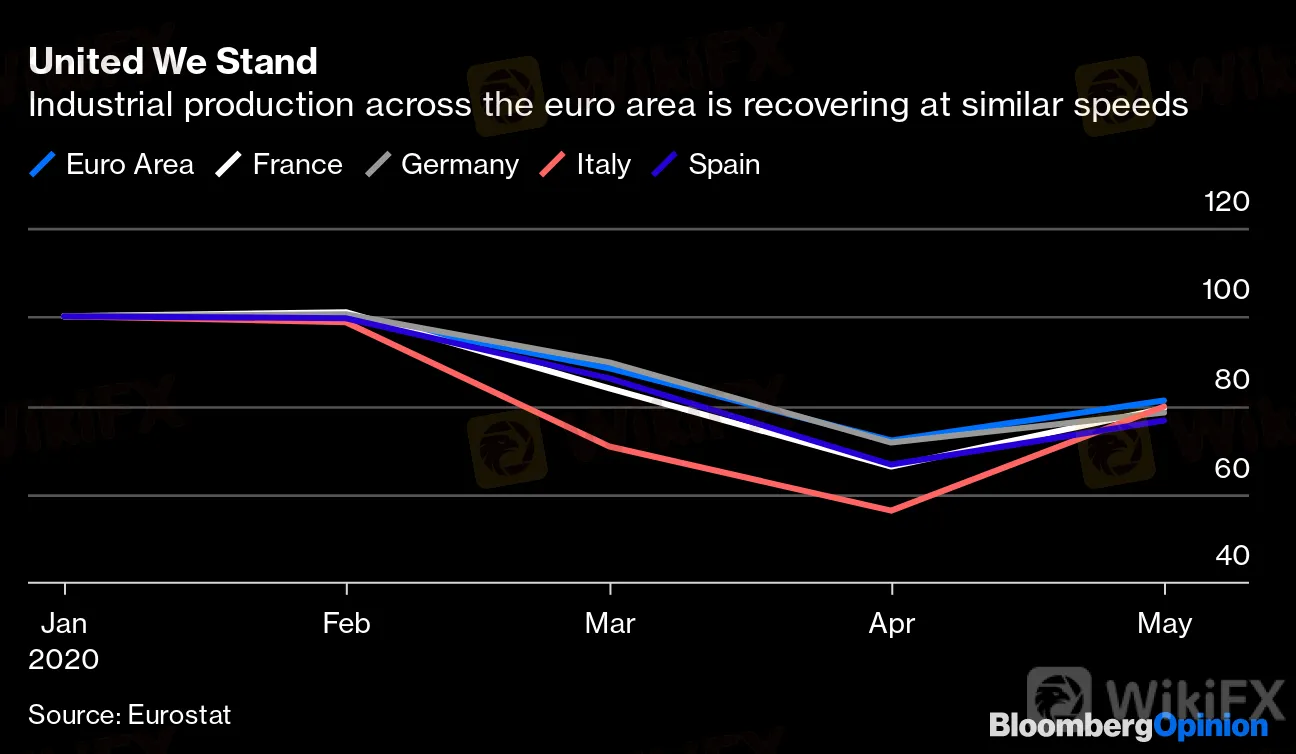

The outlook in the euro area is somewhat less gloomy than it appeared just a few weeks ago. Unlike other parts of the world, including the U.S., member states have managed to reopen their economies without triggering a second wave of infections. A string of encouraging indicators, including rising industrial production and retail sales, point to an economic rebound. The uptick is being seen across all member states, assuaging fears of a two-speed recovery: fast in some countries, such as Germany, slower in others, including Spain and Italy.

United We Stand

Industrial production across the euro area is recovering at similar speeds

Source: Eurostat

These signs will strengthen the voices of those who are fearful of the side effects of the ECBs recent interventions, which include launching a 750 billion euro ($855 billion) program of bond purchases; relaxing its buying criteria so that it can direct its firepower where it is most needed; and offering a very generous lending scheme for banks.

In particular, Jens Weidmann, president of Germanys Bundesbank, has expressed concerns that deviating from the standard rules for allocating purchases may offer governments the wrong incentives. Isabel Schnabel, a member of the executive board from Germany, has said the ECB could buy fewer bonds than anticipated.

Still, the ECB would be wise to err on the side of caution and delay any discussion on its exit strategy. The health situation remains precarious: While most countries appear to be successfully containing the virus through a strategy of local lockdowns, there is a growing fear over cases being imported from other countries where the pandemic is still raging.

There are also questions over how fast exports can rebound so long as the outlook abroad remains uncertain. Governments across Europe are shielding the labor market through unprecedented furlough schemes, but domestic demand is bound to suffer when this support ends. And it is unclear how ambitious the deal over the “recovery fund” European leaders are set to negotiate over the weekend will be, given the divisions between member states.

Given all this, it is very unlikely that inflation will return close to the ECBs target of just below 2% anytime soon.

After a shaky start, the ECB has given the euro zone all the help it needs to mitigate a catastrophic downturn and maintain financial stability. However, the recovery is still in its infancy, and numerous threats to it remain. Lagarde shouldn‘t give in to the overly optimistic. It’s best to be content with staying the course.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Geopolitical Events: What They Are & Their Impact?

WikiFX

WikiFXVolkswagen agrees deal to avoid Germany plant closures

WikiFXTop 10 Trading Indicators Every Forex Trader Should Know

WikiFXWikiEXPO Global Expert Interview: Simone Martin—— Exploring Financial Regulation Change

WikiFXTradingView Launches Liquidity Analysis Tool DEX Screener

WikiFXMultiBank Group Wins Big at Traders Fair Hong Kong 2024

WikiFX'Young investors make investment decisions impulsively to keep up with current trends' FCA Reveals

WikiFXWhy Do You Feel Scared During Trade Execution?

WikiFXCySEC Settles Compliance Case with Fxview Operator Charlgate Ltd

WikiFXScope Markets Review: Trustworthy or Risky?

WikiFXCurrency Calculator