简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Coronavirus investing strategy, how to trade next stock market crash - Business Insider

Abstract:History shows that stocks are likely to return to their lows before a full recovery kicks in, the strategists said.

The Cboe Volatility Index — or VIX, also known as the market's fear gauge — has retreated from a record high in recent weeks as stocks have recovered from their recent lows. Bank of America derivatives strategists found that this commonly cited index does not paint the full picture of what to expect in the months ahead. They believe stocks are likely to retest the lows, and recommend a hedge that bets on lower equities and a higher gold price.Click here for more BI Prime stories.

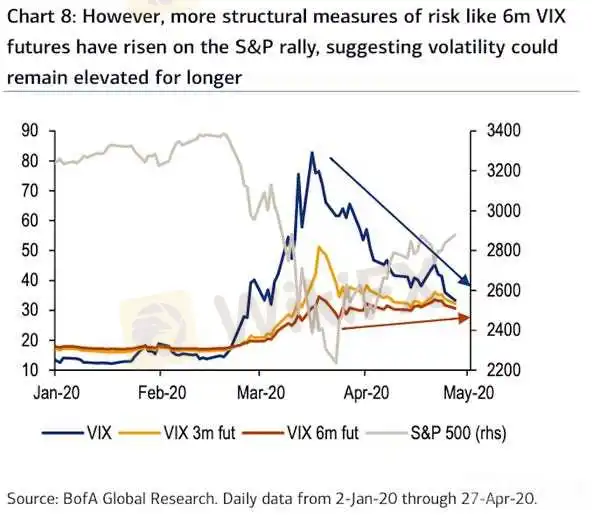

The fastest bear market in history still has more drama up its sleeve, according to derivatives strategists at Bank of America. A counterpoint can be found in the CBOE Volatility Index, or VIX, which reflects traders' future expectations for stock fluctuations. It is widely known as the market's fear gauge and tends to move in the opposite direction to the S&P 500. When the benchmark index experienced its fastest drop in record mid-March, the VIX mirrored it with a spike above 82, its highest level since November 2008. It has since rolled back to near 34, and the decline from the March 16 peak through April 27 was one of the fastest in history, according to data compiled by Bank of America.But this decline is masking other indicators that suggest the coronavirus crisis will trigger more volatility, the bank's strategists including Gonzalo Asis said in a recent note. They found that longer-dated volatility futures, including contracts that expire in six months, were rallying even as the popular spot-dated VIX was declining.

This suggests traders are betting that elevated volatility will persist.

Bank of America

A closer look into the historical relationship between the spot VIX and six-month futures adds more heft to their conclusion. There have been 105 days since 1990 when the VIX closed above 30 six months after it first crossed that level. However, only three of those days were outside of bear markets, indicating that an elevated VIX — like the one we have now — is historically more prevalent during bear markets. “Assuming VIX futures markets are pricing in this fact, the 6th VIX future trading above 30 suggests the expectation is that the bear market is likely not over,” Asis said.

He added, “our view remains that US equities are in a bear market rally and that they are likely to retest the lows before a full recovery, a view supported by strong historical evidence.”Hedge a sell-off with goldIt is prudent for investors to hedge the downside risk in stocks, Asis said. His recommendation to add portfolio protection by executing trades that wager on a rise in the price of gold, via the SPDR Gold Trust exchange-traded fund. “To cheapen equity hedges, we like trades that are both short equities and long gold, such as SPX puts contingent on gold higher and SPX down/gold up dual digitals,” he said. Investors who had counted on gold as a hedge during the recent plunge in stocks may be surprised at this recommendation since the precious metal also fell 13%.

Asis explained that gold sold off with stocks in an environment of “peak panic” — and it was not the first time. During the initial meltdowns of 1987, 2002, and 2008, gold also failed as a hedge in the early rush to sell. But during subsequent declines that were driven less by panic, gold was bid up as a safe-haven asset. “Our commodity strategists expect substantially more upside over the near- and medium-term as 'the Fed can't print gold', raising last week their 2020YE average price to $1,800/oz. and their 18-month gold target from $2,000 to $3,000/oz,” Asis added.With that in mind, his two trade recommendations are listed below verbatim:1. (Hybrid): Buy SPX Sep 2500 put (87%) contingent on GLD /> 180 (111%) for 0.75% (80% disc., ref. 2878.48, 161.56)

Best for a more bearish equity view. The 2500 SPX strike is 11% above Mar lows. The 180 GLD strike corresponds to ~$1,900/oz., near all-time highs & in line with our commodity strategists' $1,800 $/oz. avg. price by year end2. (Dual digital): Buy Sep SPX 105% for a 10-to-1 payout (ref. 2878.48, 161.56)Best for a moderately bearish equity view. Roughly corresponds to SPX 2675 and gold at $1,800/oz.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

Breakthrough again! Gold breaks through $2530 to set a new record high!

Spot gold continued its record-breaking rally as investors gained confidence that the Federal Reserve might cut interest rates in September and gold ETF purchases improved. The U.S. market hit a record high of $2,531.6 per ounce

Historic Moment: Gold Surges Above $2,500 Mark, Forging Glory!

Boosted by the weakening of the US dollar and the expectation of an imminent rate cut by the Federal Reserve, spot gold broke through $2,500/ounce, setting a new record high. It finally closed up 2.08% at $2,507.7/ounce. Spot silver finally closed up 2.31% at $29.02/ounce.

Weekly Analysis: XAU/USD Gold Insights

Gold prices have been highly volatile, trading near record highs due to various economic and geopolitical factors. Last week's weak US employment data, with only 114,000 jobs added and an unexpected rise in the unemployment rate to 4.3%, has increased the likelihood of the Federal Reserve implementing rate cuts, boosting gold's appeal. Tensions in the Middle East further support gold as a safe-haven asset. Technical analysis suggests that gold prices might break above $2,477, potentially reachin

【MACRO Insight】Monetary Policy and Geopolitics - Shaping the Future of Gold and Oil Markets!?

In the ever-evolving global economy, the intertwining influences of monetary policy and geopolitical factors are reshaping the future of the gold and crude oil markets. This spring, the gold market saw a significant uptrend unexpectedly, while Brent crude oil prices displayed surprising stability. These market dynamics not only reflect the complexity of the global economy but also reveal investors' reassessment of various asset classes.

WikiFX Broker

Latest News

ASIC Sues Binance Australia Derivatives for Misclassifying Retail Clients

WikiFX

WikiFXWikiFX Review: Is FxPro Reliable?

WikiFXMalaysian-Thai Fraud Syndicate Dismantled, Millions in Losses Reported

WikiFXTrading frauds topped the list of scams in India- Report Reveals

WikiFXAIMS Broker Review

WikiFXThe Hidden Checklist: Five Unconventional Steps to Vet Your Broker

WikiFXYAMARKETS' Jingle Bells Christmas Offer!

WikiFXRevolut Leads UK Neobanks in the Digital Banking Revolution

WikiFXFusion Markets: Safe Choice or Scam to Avoid?

WikiFXSEC Approves Hashdex and Franklin Crypto ETFs on Nasdaq

WikiFXCurrency Calculator