简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

【MACRO Insight】Triggering Fed Rate Cut Expectations and Yen Volatility

Sommario:As of October 4, 2024, the London gold price has risen by 3.3% since the Fed‘s interest rate cut on September 18, and has risen by 28.6% so far this year. The strength of gold prices is not entirely a

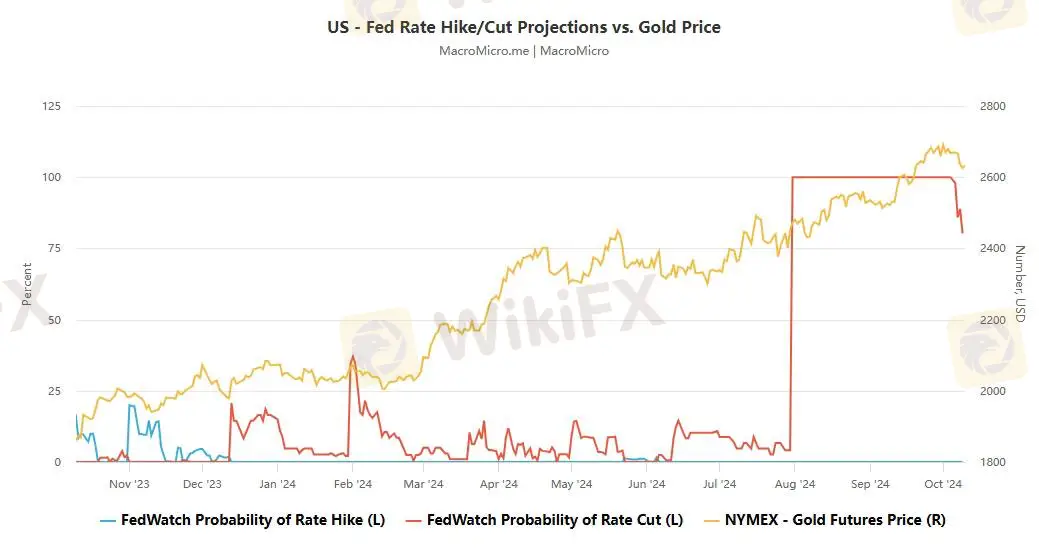

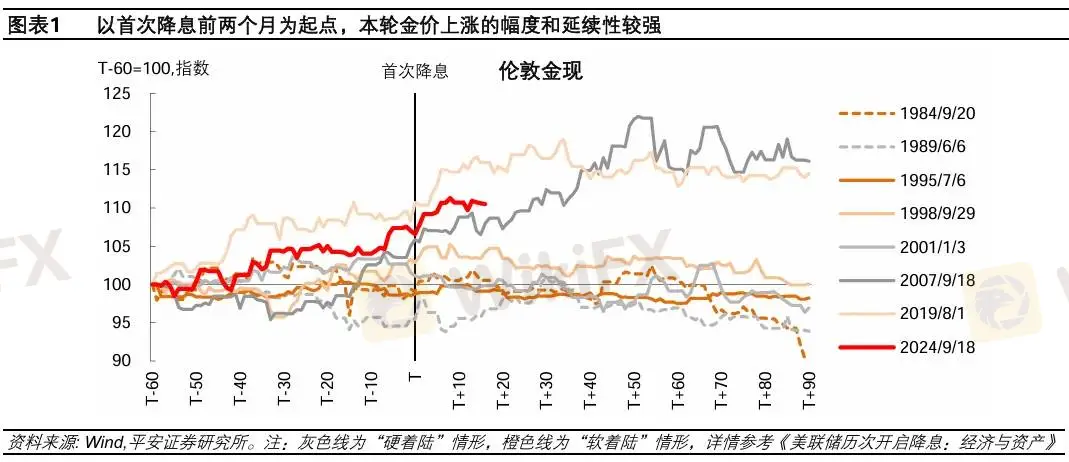

As of October 4, 2024, the London gold price has risen by 3.3% since the Fed‘s interest rate cut on September 18, and has risen by 28.6% so far this year. The strength of gold prices is not entirely attributed to the Fed’s interest rate cut. The Feds interest rate cut is usually conducive to the rise in gold prices, but considering that gold prices have clearly strengthened before the current rate cut, the strong performance after the rate cut still exceeded expectations.

One month before this round of rate cuts, the 10-year Treasury bond futures price and the US dollar index rose by 1.5% and fell by 1.4%, respectively, which basically matched the 2.5% increase in the London gold spot price. However, in the 13 trading days after the rate cut, the 10-year Treasury bond price weakened (the 10-year Treasury bond interest rate rebounded by 33BP and the real interest rate rebounded by 22BP), and the US dollar index rose by 1.5%, which could hardly explain the 3.7% increase in the gold price.

Since 2022, the traditional negative correlation between gold prices and 10-year U.S. Treasury bond real interest rates has continued to weaken, showing an overall “strong gold and weak bonds” pattern. Traditional analytical frameworks based on the U.S. dollar system, such as the World Gold Council's five-factor gold price return model (GRAM), are difficult to explain the degradation of the correlation between gold prices and U.S. Treasury bonds. Since 2022, the “over-inflation” of gold prices reflects the market's concerns about U.S. fiscal policy and the credit of the U.S. dollar.

Since 2024, the US government debt has continued to expand, and the pressure of interest payments has risen rapidly. The upcoming presidential election does not change the outlook for fiscal expansion. Recently, concerns about US fiscal problems are still intensifying: first, the US government is facing the risk of shutdown again, and the fiscal risk has triggered Moody's warning; second, the geopolitical situation in the Middle East and other regions continues to be tense, the conflict between Lebanon and Israel has escalated, and US military spending is expected to rise.

The hot gold trade is seeing some pullbacks. On Wednesday, gold prices fell for the sixth consecutive trading day, hovering near the two-week low hit in the previous session, as market participants reduced expectations for a big rate cut and turned their attention to the Federal Reserve minutes and inflation data. Kathryn Rooney Vera, chief market strategist at StoneX, pointed out that “gold is fascinating, and I think people are definitely starting to hedge risks, but now the gold rally is starting to look 'too exhausted', and I would also predict that it will have some pullbacks and take some gains into the bag.”

Gold is one of the best performing assets this year. So far this year, gold prices have soared 27% to above $2,600 an ounce. On September 26, gold prices hit an all-time high of $2,694 an ounce. In comparison, the S&P 500 has risen 20% this year. There are many factors driving the surge in gold demand, such as geopolitical and economic instability, which tend to trigger market demand for safe-haven assets such as gold. In addition, some experts pointed out that the weakening of the US dollar and the Federal Reserve's tendency to cut interest rates have further supported gold prices.

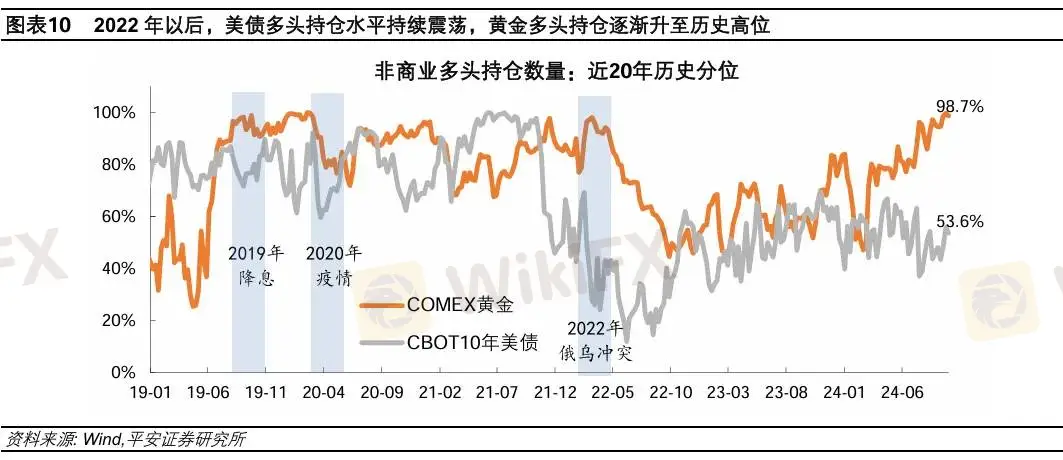

Against the backdrop of the Fed's interest rate cuts, gold is more attractive than U.S. Treasuries in this round, making it likely to perform more strongly. However, gold prices may face certain adjustment risks in the short term. First, bullish gold positions continue to be crowded, and “fear of heights” may affect the sustainability of gold price increases. The proportion of non-commercial long positions in COMEX gold has remained above 60% since June. In the past two decades, the proportion has not been above 60% for many times, and the longest period has not exceeded 4 months. Secondly, the recent rebound in U.S. Treasury bond interest rates has gradually accumulated pressure on gold prices. Although the correlation between gold prices and U.S. Treasury (real) interest rates is not as good as before, it has not disappeared.

Finally, with the improvement of China's economic prospects, Asian funds' demand for gold allocation may cool down. Since March this year, with the 10-year Chinese bond interest rate breaking the 2.3% mark, the price of gold has accelerated its rise. Behind this is the significant increase in the demand for gold allocation in China and Asia. In the current complex market environment, the future trend of gold prices is full of uncertainty. Both bulls and bears are looking for opportunities, and geopolitical tensions and the upcoming US election may bring more volatility to the market.

Disclaimer:

Le opinioni di questo articolo rappresentano solo le opinioni personali dell’autore e non costituiscono consulenza in materia di investimenti per questa piattaforma. La piattaforma non garantisce l’accuratezza, la completezza e la tempestività delle informazioni relative all’articolo, né è responsabile delle perdite causate dall’uso o dall’affidamento delle informazioni relative all’articolo.

WikiFX Trader

VT Markets

EC Markets

Vantage

IC Markets Global

IQ Option

OANDA

VT Markets

EC Markets

Vantage

IC Markets Global

IQ Option

OANDA

WikiFX Trader

VT Markets

EC Markets

Vantage

IC Markets Global

IQ Option

OANDA

VT Markets

EC Markets

Vantage

IC Markets Global

IQ Option

OANDA

Rate Calc