简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

U.K. Chancellor Sunak Urged to Treat Coronavirus Borrowing as War Debt

Abstract:U.K. Chancellor of the Exchequer Rishi Sunak is being asked by members of the ruling Conservative Party to take his time to pay off the record debt the country is racking up as it tries to weather the coronavirus pandemic. By that, they mean decades.

U.K. Chancellor of the Exchequer Rishi Sunak is being asked by members of the ruling Conservative Party to take his time to pay off the record debt the country is racking up as it tries to weather the coronavirus pandemic. By that, they mean decades.

With the economy on course for its deepest recession for at least a century, the government is now paying the wages of more than 10 million workers to stave off mass unemployment.

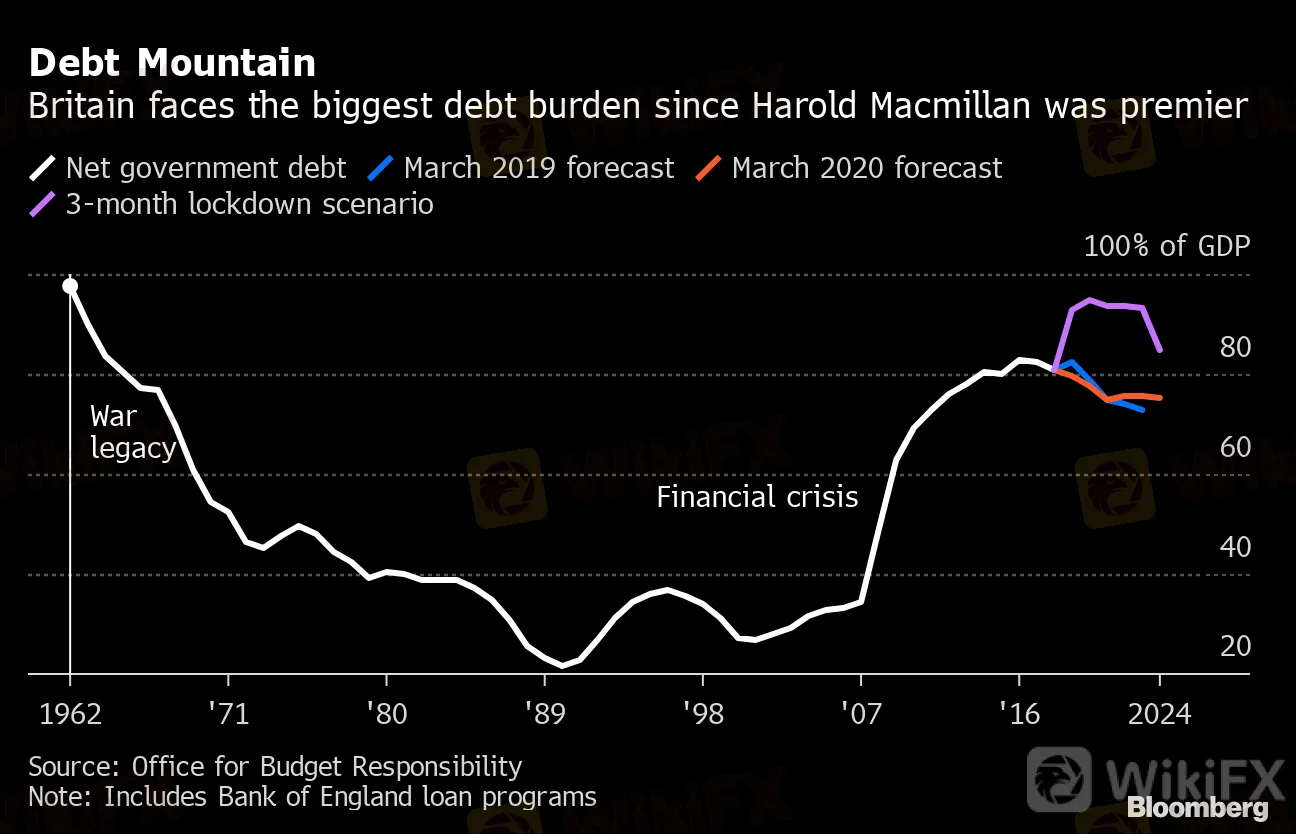

The cost of such emergency measures, together with the hit to tax revenue triggered by the slump, is set to push the budget deficit to the widest since World War II, according to the Office for Budget Responsibility. The national debt is on course to hit almost 100% of gross domestic product, a level not seen since the days of Prime Minister Harold Macmillan and the Profumo scandal.

For Conservative lawmakers, a rush to cut spending and pay off the debt quickly could choke any recovery in the economy, imperiling their chances of re-election. So the party that put the country through the biggest fiscal squeeze in peacetime after the financial crisis is coming round to the idea that the U.K. will have to live with record debt for years to come -- just as a succession of governments found after 1945.

“There‘s talk about whether the coronavirus debt should be treated like Second World War debt, where it will sit on the national books much longer,” said Nicky Morgan, a Tory member of the House of Lords who served in Prime Minister Boris Johnson’s cabinet until February. “I think it should.”

The U.K. only paid off the last of its World War II debts to the U.S. at the end of 2006. In 2014, then Chancellor of the Exchequer George Osborne announced plans to pay off debt dating back to the South Sea Bubble of 1720, as well as World War I. By then, those borrowings had been consolidated into perpetuals -- bonds with no fixed maturity.

Debt Mountain

Britain faces the biggest debt burden since Harold Macmillan was premier

Source: Office for Budget Responsibility

Note: Includes Bank of England loan programs

With few in Johnsons party advocating the sort of spending cuts deployed by David Cameron and Osborne, and the coronavirus crisis reviving questions about inequality, the government is expected to double down on its pre-virus pledge to stimulate the economy by boosting infrastructure spending.

“Nobody in their right mind is comfortable with the debt -- but I certainly don‘t take, as a Conservative, a view that we should not be spending money,” said Michael Fabricant, a Tory lawmaker. “It’s inevitable that we will have to live with high levels of debt for some time to come.”

Steve Baker, another Tory backbencher, told a webinar organized by the Institute of Economic Affairs that while there is a “need to think about future generations” there is little appetite for more austerity, and tax rises would be “controversial.”

“You just accept that you‘re going to be paying off this debt in small installments for many decades to come,” David Lidington, who served as deputy to Johnson’s predecessor, Theresa May.

That willingness to kick the issue into the long grass is evidence of how effective the Bank of Englands vast bond-buying plan has been in keeping borrowing costs low and stable for the government.

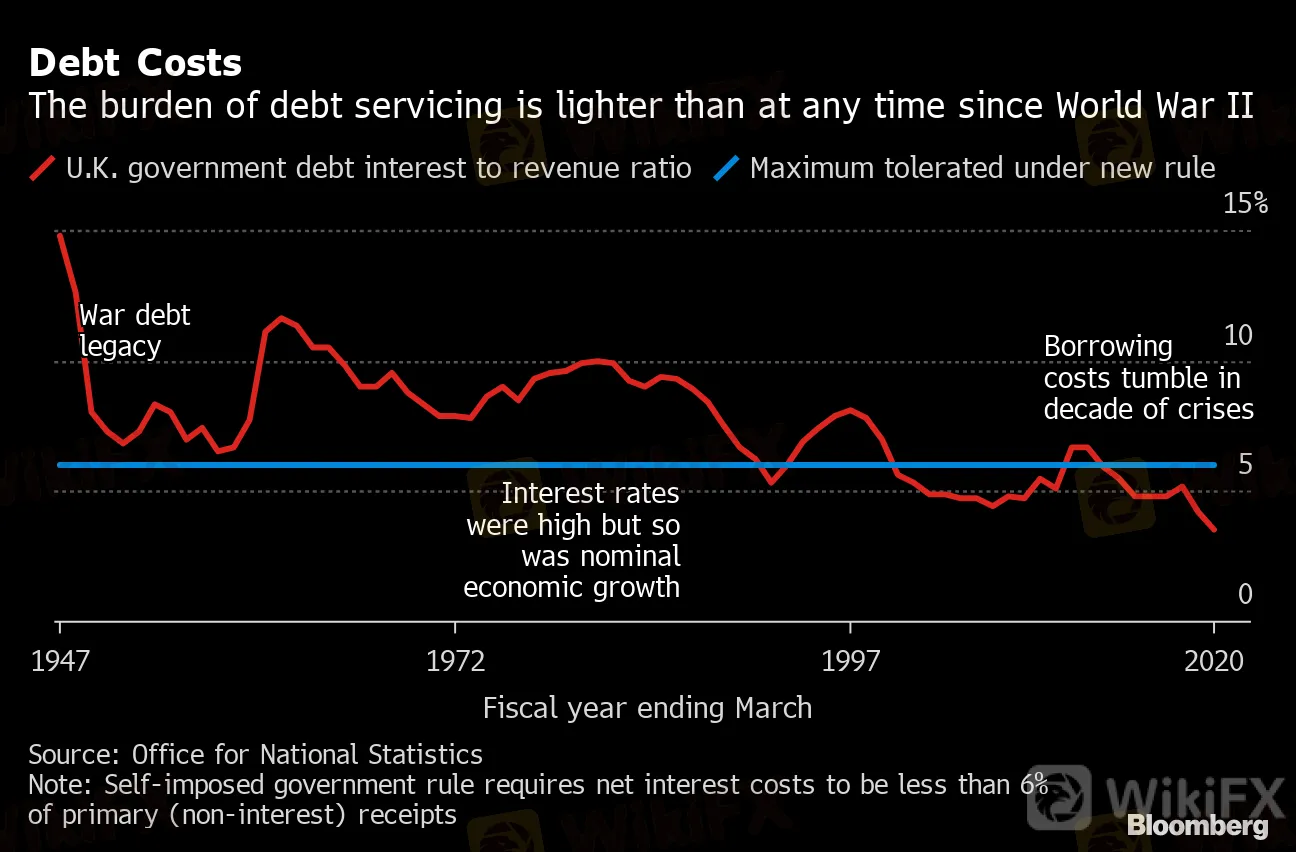

Debt Costs

The burden of debt servicing is lighter than at any time since World War II

Source: Office for National Statistics

Note: Self-imposed government rule requires net interest costs to be less than 6% of primary (non-interest) receipts

Even though government borrowing is far higher than it was before the financial crisis, the U.K. can still borrow for 10 years at about 0.3%, down from 5% in 2008.

Gilt sales are due to total 225 billion pounds ($287 billion) between April and July, with the final total for this fiscal year set to soar well above the record set in the financial crisis.

So far, the governments sales have met with strong demand from investors -- in part because the central bank has also been buying a vast amount of gilts in the secondary market. The cost to the Treasury is the interest rate charged on the BOE reserves used to finance that buying, rather than the usual coupon payments.

That means 570 billion pounds is currently being financed at an annual rate of 0.1%, an amount that is due to hit 625 billion pounds by July and is expected to increase further. The flip-side is that debt-servicing costs are far more sensitive to changes in the BOEs key rate.

“It would be a mistake to think that just because interest rates are low, over the very long term they‘re necessarily remaining low,” Philip Hammond, who served as chancellor of the exchequer under May, told lawmakers last week. “I personally wouldn’t be comfortable with a strategy that said were happy for debt to run to 100 plus percent of GDP, and just to leave it there forever.”

For Stephen King, senior economic adviser at HSBC Holdings Plc, low interest rates may be the only thing counting in the U.K.s favor, with debt levels already high and globalization slipping into reverse. Governments, he says, only have three ways out of debt in the end: Higher inflation, something that would be unpopular with elderly savers, default -- or higher taxes.

“To say were just going get the billionaires to pay for it is a cop out,” Osborne told the Treasury Committee last week. He predicts this parliament will be “completely dominated” by debates over the economy and public finances. “That is what the politics is going to be all about.”

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

BI Apprehends Japanese Scam Leader in Manila

WikiFX

WikiFXBitcoin in 2025: The Opportunities and Challenges Ahead

WikiFXJoin the Event & Level Up Your Forex Journey

WikiFXIs There Still Opportunity as Gold Reaches 4-Week High?

WikiFXBitcoin miner\s claim to recover £600m in Newport tip thrown out

WikiFXGood News Malaysia: Ready for 5% GDP Growth in 2025!

WikiFXHow to Automate Forex and Crypto Trading for Better Profits

WikiFXBreaking News! Federal Reserve Slows Down Interest Rate Cuts

WikiFXBeware: Pig Butchering Scam Targeting Vulnerable Individuals

WikiFXThis Economic Indicator Sparks Speculation of a Japan Rate Hike!

WikiFXCurrency Calculator