简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

US Dollar Down, S&P 500 Shows Weakness After Decidedly Dovish Fed

Abstract:The US Dollar fell as the S&P 500 trimmed sharp gains on a more dovish Fed that downgraded economic projections and rate hike estimates. AUD/USD may rise on a rosy jobs report.

Asia Pacific Market Open Talking Points

The US Dollar fell on dovish Fed and softer economic projections

S&P 500 jawboned, quickly trimming sharp gains on the FOMC

NZD/USD unexpectedly rose on lackluster GDP, AUD eyes jobs data

Find out what the #1 mistake that traders make is and how you can fix it!

Key FX Developments Wednesday

The US Dollar underperformed against its major counterparts on Wednesday after a relatively dovish Fed rate decision. Heading into the announcement, the markets were pessimistic with Fed funds futures pricing in a 25% chance of a cut by the end of this year. This would entail dropping the 2 rate hikes policymakers projected for 2019 back in December.

That turned out to be the case, but in the medium-term the updated dot plot (a chart that shows each officials forecast for rates in the future) still alluded to one hike in 2020. What seemed to carry more weight in the FOMC announcement, and sending local front-end government bond yields lower, was a more pessimistic downgrade in economic projections than expected.

Wall Street and the S&P 500 soared on the announcement. This is because a pause in the central banks tightening cycle bodes well for equities. What is more interesting is that just two hours after the Fed, the S&P 500 was back to square one as it trimmed all its gains on the FOMC. The reality that financial markets face is that such a dramatically dovish shift in arguably the most influential central bank is not without its consequences.

Elsewhere, the British Pound also weakened as markets met UK Prime Minister Theresa Mays request to extend the Brexit deadline by three months with skepticism. Meanwhile, the anti-risk Japanese Yen and Swiss Franc were some of the best-performing majors as markets seem quite cautious. European equities did close lower before Wall Street did the same.

Thursdays Asia Pacific Trading Session

As markets transitioned into Thursdays Asia Pacific trading session, the New Zealand Dollar puzzlingly got a boost from lackluster local fourth quarter GDP data. While the year-on-year rate of growth slowed, markets seemed to focus more on the in-line 0.6% quarter-on-quarter outcome. This may have led investors to believe that perhaps the nation could remain resilient in the short-term as world output slows.

Ahead, the Australian Dollar looks to February‘s jobs report. Lately, economic data from Australia has been tending to outperform relative to economists’ expectations. A rosy outcome may diminish RBA rate cut bets, which are more aggressive than those priced in for the Federal Reserve. That may send AUD/USD higher. But follow-through will depend on how Asia stocks interpret the Fed and Wall Streets trading session.

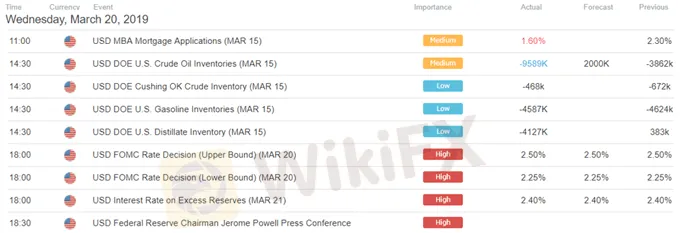

US Trading Session Economic Events

Asia Pacific Trading Session Economic Events

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

KVB Market Analysis | 30 August: JPY Strengthens Against USD Amid Strong Q2 GDP and BoJ Rate Hike Speculation

The Japanese Yen (JPY) strengthened against the US Dollar (USD) on Thursday, boosted by stronger-than-expected Q2 GDP growth in Japan, raising hopes for a BoJ rate hike. Despite this, the USD/JPY pair found support from higher US Treasury yields, though gains may be capped by expectations of a Fed rate cut in September.

NFP Hammers Dollar to 4 Months Low

The aftermath of the Japanese yen's strengthening has manifested in significant dips across multiple markets, including equities, commodities, and various currencies. The yen has erased all its 2024 losses against the dollar, moving towards the 145.00 mark. The dollar index (DXY) has fallen to its lowest level since March, hovering above the $103 mark.

KVB Today's Analysis: Gold Bullion Gains Strength Amid Fed's Dovish Stance on Interest Rates

Fed officials have indicated they are prepared to cut interest rates if necessary, though there is no immediate need. This dovish stance has been viewed positively by the markets, leading to increased buying pressure on gold. Despite ongoing inflationary risks, market expectations of a rate cut in June have risen to 66.3% (up 3% since the PCE release). Lower interest rates could enhance the appeal of non-yielding gold.

Yen Resurgence! Will Next BoJ Week Sustain the Rally?

The U.S. Conference Board reported a slight decline in the US Consumer Confidence Index (CCI) for June 2024, dropping to 100.4 from 101.3 in May. The Bank of Japan (BoJ) opted to keep its key short-term interest rate steady at 0.10% for June 2024, in line with market expectations. At its June 2024 meeting, the Federal Reserve decided to keep the federal funds rate unchanged at 5.50%. In June 2024, the Bank of England (BoE) decided to keep the interest rate at 5.25% unchanged. This decision...

WikiFX Broker

Latest News

Will Gold Break $2,625 Amid Fed Caution and Geopolitical Risks?

WikiFX

WikiFXECB Targets 2% Inflation as Medium-Term Goal

WikiFXNew Year, New Surge: Will Oil Prices Keep Rising?

WikiFXPH SEC Issues Crypto Guidelines for Crypto-Asset Service Providers

WikiFXFTX Chapter 11 Restructuring Plan Activated: $16 Billion to Be Distributed

WikiFXThink Before You Click: Malaysian Loses RM240,000 to Investment Scam

WikiFXBithumb CEO Jailed and Fined Over Bribery Scheme in Token Listing Process

WikiFXWikiFX Review: Something You Need to Know About Saxo

WikiFXIs PGM Broker Reliable? Full Review

WikiFXTerraform Labs Co-founder Do Kwon Extradited to the U.S. to Face Fraud Charges

WikiFXCurrency Calculator